Policy

Development Impact Week 2023

See my talk on how using large administrative data provides a better lens for governments to design public policy

Selected Policy Notes & Reports

This report examines the design and implementation of Devolve ICMS, a state-level personalized VAT cashback program in Rio Grande do Sul, Brazil, through the lens of the World Bank's G2Px framework. Using administrative data, a representative beneficiary survey, and qualitative interviews, it provides an in-depth assessment of the systems and infrastructure supporting the program, illustrating key elements needed to implement a modern VAT cashback scheme.

This note is part of a collaboration between the World Bank's DECRG and DIME and the Dominican Pension Superintendency (SIPEN). It leverages complete administrative records of pension contributions—a matched employer-employee dataset—to provide insight on the performance of the pension system and guide pension policy in the DR and beyond.

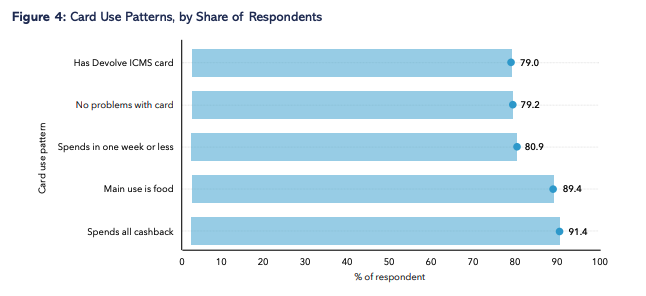

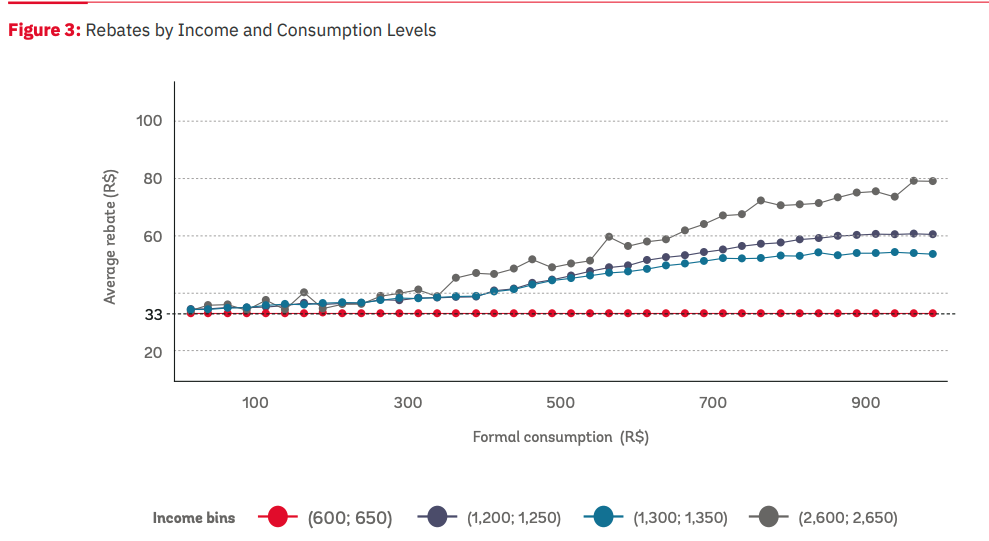

VAT Cashback Programs in Practice: The Case of Devolve-ICMS in Rio Grande do Sul, Brazil

This note describes the Devolve-ICMS program, an innovative VAT cashback initiative aimed at refunding taxes to low-income households in Rio Grande do Sul, Brazil. Using administrative records, it documents key stylized facts: even the poorest households consume in formal stores, lower-income families consume more as a share of income, and formal consumption is higher for female-headed households.

Income Taxation of the Top Earners in Honduras: Linking Personal and Corporate Taxes

This note examines effective income tax rates for top earners in Honduras by linking personal and corporate income tax data. Over 50% of total comprehensive income for the top 0.05% of earners comes from undistributed corporate profits, and the effective tax rate for the top 0.01% hovers around 25%—relatively flat compared to high-income countries.

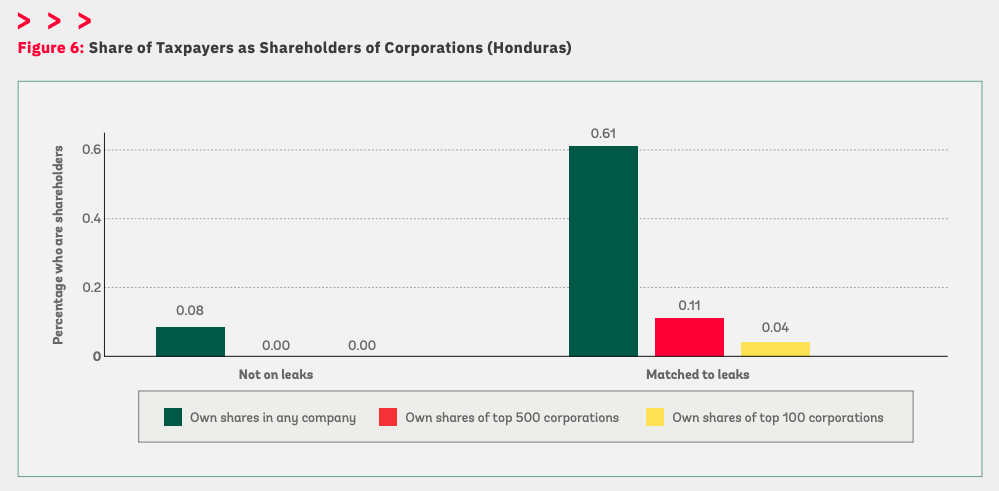

Offshore Data Leaks and Tax Enforcement in Developing Countries

This note analyzes three country cases—Ecuador, Honduras, and Senegal—where the authors collaborated with national tax administrations to leverage offshore data leaks (Panama Papers, Pandora Papers) for tax enforcement. It documents the distribution of offshore company formation and provides policy recommendations for enhancing personal income tax enforcement.

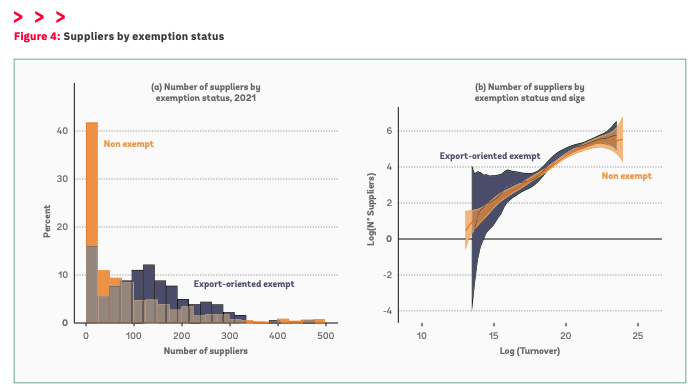

Firms' Networks Under Export Exemption Regimes: Stylized Facts from Honduras

This report uses administrative tax data on firm-to-firm trade in Honduras to evaluate the integration between firms receiving export-oriented tax exemptions and the local economy. Across several dimensions, networks of firms in export-oriented regimes do not differ from those of other similarly sized firms, challenging the idea that such regimes benefit disconnected enclaves.

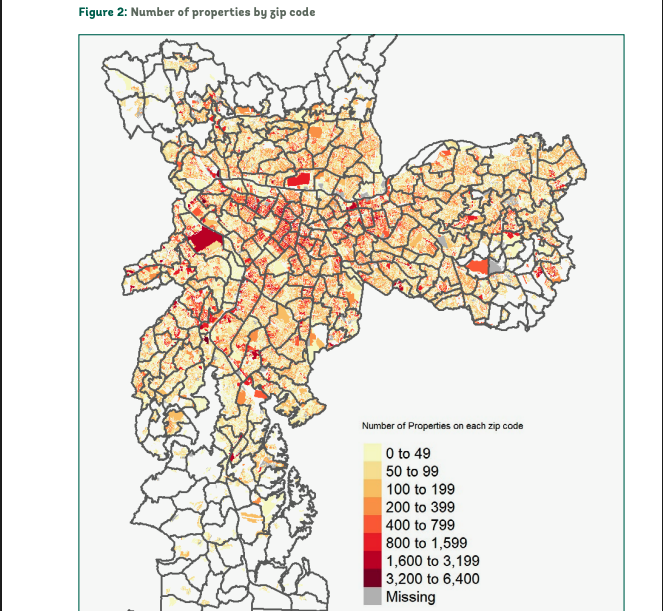

Gender and Property Taxes in São Paulo

This knowledge note provides new evidence on property ownership and taxation patterns across genders in São Paulo, the largest city in the Americas. Using microdata on all commercial and residential properties, it documents the share of property and property wealth owned by women and the implications for property taxes in the city.

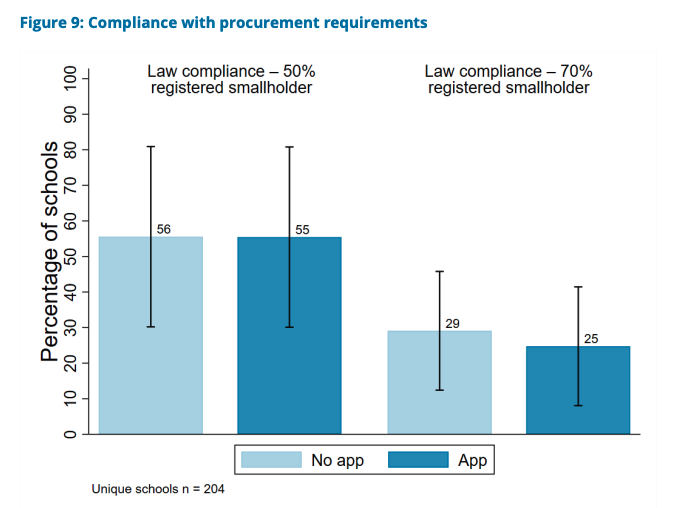

Guatemala, Home-Grown School Feeding Programme: Pilot Impact Evaluation

This pilot impact evaluation uses an RCT design to assess the impact of a digital app on school feeding programme operations in Guatemala. Despite high training participation (99% of schools), app usage was low—only 12% posted a purchase order—primarily due to internet connectivity and functionality issues.